Is It Better To Rent Than Buy a Home Right Now?

You may have seen reports in the news recently saying it’s more affordable to buy a home. And while that may be true in some markets if you just look at typical monthly payments, there’s one thing the numbers aren’t factoring in: home equity. Here’s a look at how big of an impact equity can have and why it’s worth considering as you make your decision.

The Headlines Behind the Numbers

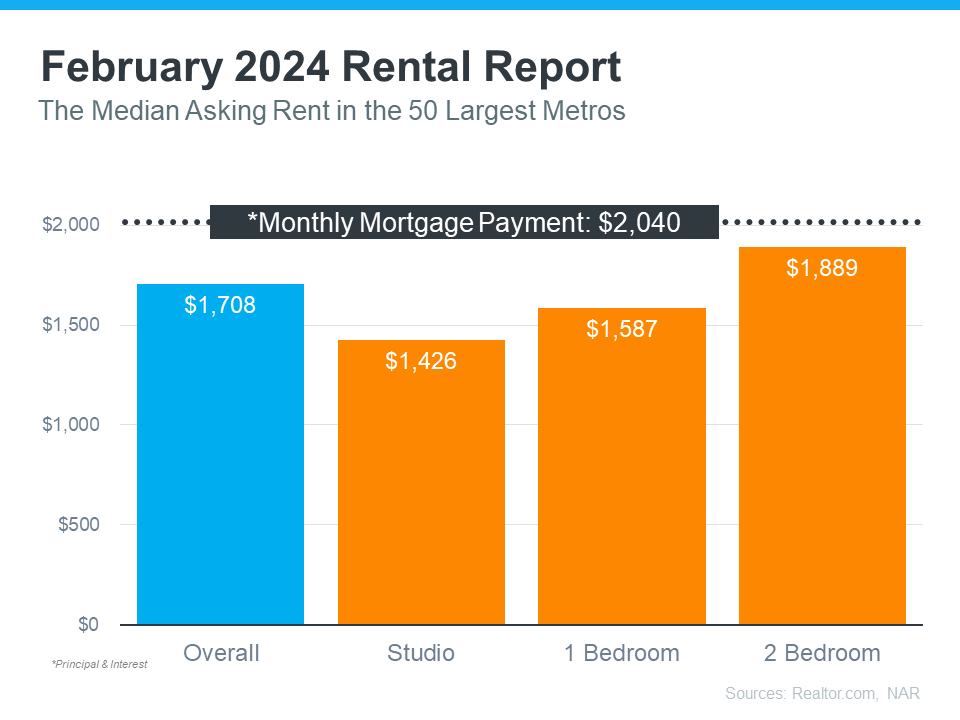

The graph below uses national data on the median rental payment from Realtor.com and median mortgage payment from the National Association of Realtors (NAR) to compare the two options. As the graph shows, especially if you’re not looking for a lot of space, it can be more affordable on a monthly basis to rent:

For a 2-bedroom home, the median monthly mortgage payment is $2,040, while median rent is $1,889—a difference of just $151 per month. But when you factor in equity, the picture changes.

How Equity Changes the Game

If you rent, your payments only cover housing costs and your landlord’s expenses. When you buy, your mortgage payment also acts as an investment, building equity over time. That equity grows faster as home values increase.

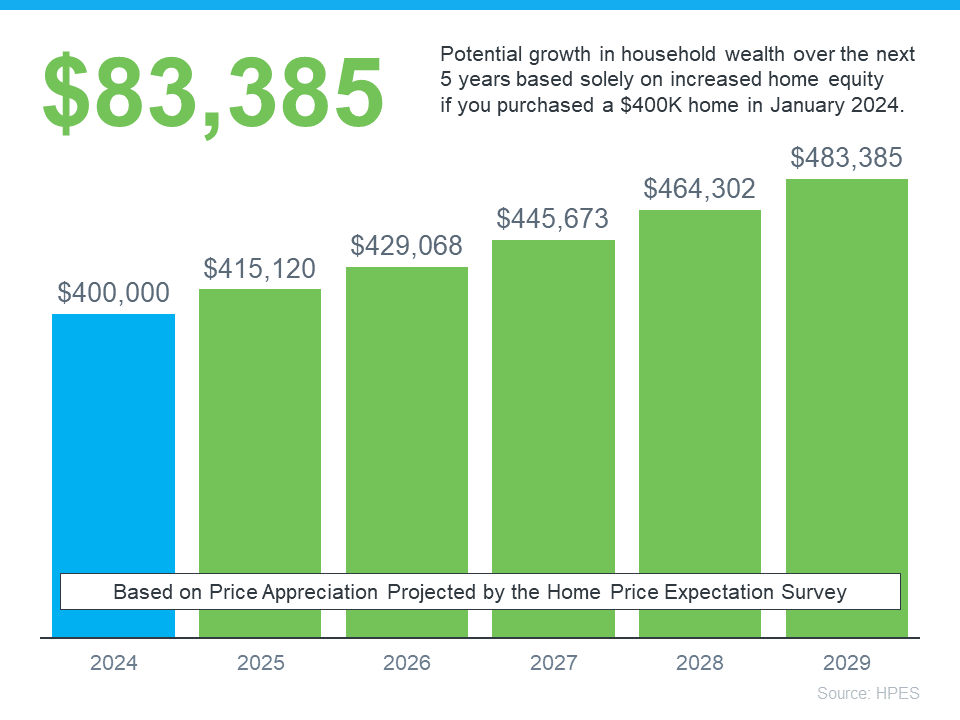

According to the latest Home Price Expectations Survey (HPES), home prices are expected to continue rising over the next five years. Here’s how equity could build based on those projections:

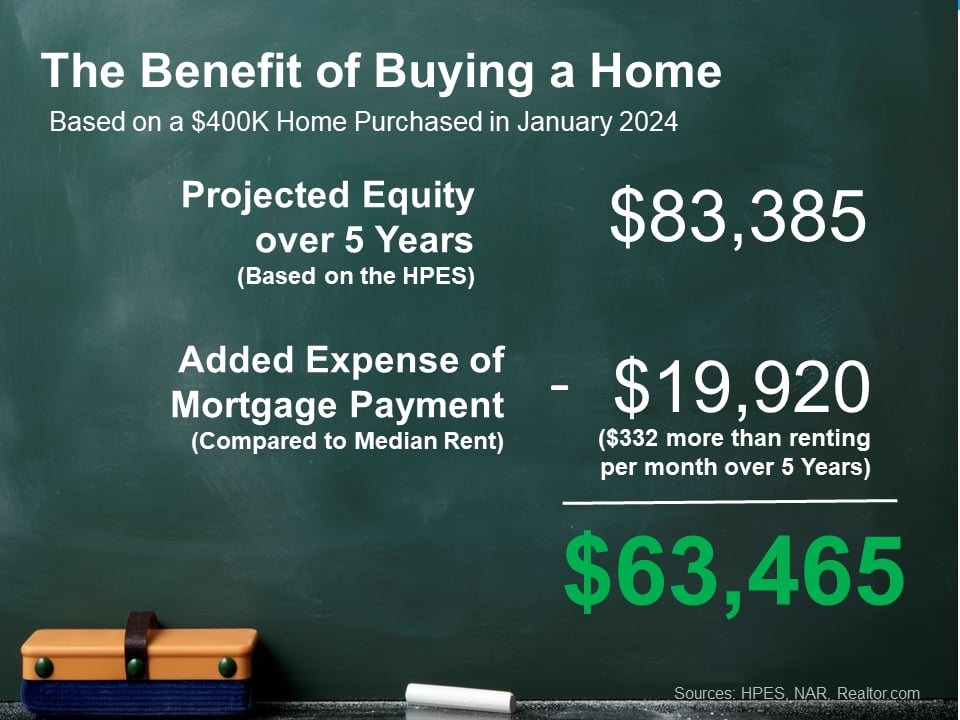

Imagine buying a home for $400,000. Based on HPES projections, living there for 5 years could grow your household wealth by over $83,000, compared to renting, using median rent:

While renting may save you a bit each month, buying gives you the long-term advantage of equity. Whether renting or buying makes more sense depends on your personal finances, but equity can make buying a stronger long-term choice.

Bottom Line

Buying a home gives you a benefit renting cannot: the chance to build equity. If you want to take advantage of long-term home price appreciation, let’s discuss your options.